THE 2028 GLOBAL INTELLIGENCE RENAISSANCE

A Bullish Rebuttal to The 2028 Global Intelligence Crisis

Foreword

The most dangerous ideas are the ones that feel inevitable.

Citrini Research published a piece that touched a nerve. They clearly articulated the anxieties I have about AI and the future economy in a way I hadn't managed to myself. They called it The 2028 Global Intelligence Crisis, a fictional macro memo written from June 2028, reconstructing how AI-driven disruption unraveled into a full-blown economic catastrophe. You should read it first. They describe a scenario where AI scales economic productivity but couples it with a fatalistically unraveling labor market — a world where the flow of capital bypasses humans entirely, as they lose the ability to provide economic value.

The bear case, briefly (seriously, read their essay): agentic AI triggers mass white-collar layoffs beginning in 2026. Displaced workers spend less. Consumer demand contracts. Companies facing margin pressure invest more in AI to cut costs further, accelerating the next round of layoffs. A negative feedback loop with no natural brake. Ghost GDP — output that appears in national accounts but never circulates through households. The $13 trillion residential mortgage market, underwritten against incomes that no longer exist, begins to crack. Private credit defaults find their way into life insurer balance sheets through offshore structures nobody fully understood until it was too late. The Fed can cut rates to zero. It cannot change the fact that a Claude agent does the work of a $180,000 product manager for $200 a month. S&P 3,500. Unemployment 10.2%. The Intelligence Displacement Spiral.

The authors got the mechanism right. But the model is incomplete. It describes one half of the ledger with forensic precision and quietly ignores the other entirely; a world with no new opportunities, where the only wielders of intelligence are gigantic corporations. This is why I started this Substack. I have felt the pull towards AI fatalism, a dystopia where humans lose their ability to provide economic value, stripped of purpose, closer than we’d like to admit.

It’s a future underestimating humanity. I don’t buy it.

Here’s what I believe instead. The developments in AI will reduce the cost of intelligence and democratize the future economy. Anyone with drive, curiosity, and grit can enter a field and compete. Those rich in free time and determination will beat those rich in capital and institutional knowledge. We may see more millionaires and maybe even billionaires created than ever before — not because they’re tech titans, but because they leveraged new tools to unlock creativity and build businesses at a rate never seen before. That is what an Intelligence Renaissance looks like.

So I wrote the other half. The bull case. Same format. Same voice. Same starting conditions. Different equilibrium. Not because the disruption doesn’t happen, but because the countervailing forces the bear model ignores turn out to matter for what happens next to humanity.

What follows is a fictional macro memo from the same June 2028 — the one where the canary didn’t die.

— A Future Bull

First, if you enjoy these posts, consider subscribing and becoming a part of our growing community!

The Consequences of Abundant Intelligence

March 1st, 2026 June 30th, 2028

The unemployment rate printed 6.2% this morning, the fourth consecutive monthly decline from the 7.8% peak we hit in Q3 2027. The market rallied 1.4% on the number. The S&P 500 is now up 14% from the lows, within striking distance of the October 2026 highs that seemed so distant six months ago.

Traders are cautiously relieved. Eighteen months ago, the same print would have triggered a short squeeze and fresh mania. Today it is absorbed with something approaching appropriate skepticism. That is healthy.

Two years. That is all it took to get from “contained and sector-specific” to an economy that no longer resembles the one any of us grew up in — and then, unexpectedly, to an economy that has begun to resemble something none of us had quite imagined before. This quarter’s macro memo is our attempt to reconstruct the sequence. A post-mortem on the fears that, in crucial respects, did not materialize.

The fears were not irrational. We shared many of them. What the bears got right about the mechanism, they got wrong about the equilibrium.

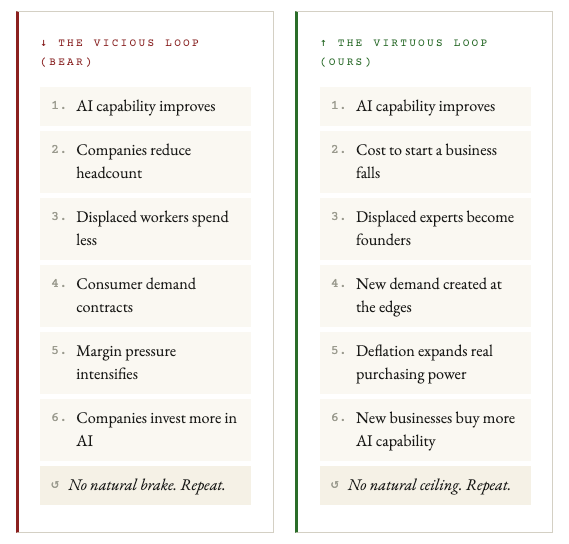

The Two Loops

The bear scenario was built around a feedback loop with no natural brake. We argued then, and document now, that an equal and opposite loop was always present — suppressed in their model, but real in the economy.

The Two Ledgers

The bear model described one half of the economic ledger with precision. It quietly omitted the other. Here are both columns, side by side.

The Euphoria Was Palpable — And Then So Was the Fear

By October 2026, the S&P 500 flirted with 8,000. The initial wave of layoffs due to human obsolescence began in early 2026 (foreboding) and did exactly what layoffs are supposed to do. Margins expanded. Earnings beat. Stocks rallied. Record-setting corporate profits were funneled right back into AI compute.

Then the narrative shifted. The unemployment rate began its measured rise. White-collar job openings collapsed. A consensus formed, quickly and with considerable analytical force, that this disruption was different — that AI was a general intelligence which would absorb the jobs it created, that the feedback loop had no natural brake, that the velocity of money would flatline as machines replaced the workers who drove consumer spending.

We published our own concerns. In January 2027, we argued that the U.S. economy was essentially a white-collar services economy, and that the businesses AI was chewing up were not tangential to GDP — they were GDP. We were right about the mechanism.

We were wrong about the equilibrium.

The bears built an elegant closed-loop model. AI improves, companies need fewer workers, displaced workers spend less, companies invest more in AI, AI improves. They asked, correctly, how much money machines spend on discretionary goods. The answer, zero, was supposed to be the kill shot.

What the model missed was the other half of the ledger. It focused with forensic precision on what was being destroyed, and almost none at all on what was simultaneously being created. Every great disruption has two faces. The bear memo described one of them brilliantly. This memo describes the other.

How It Started

In late 2025, agentic coding tools took a step-function jump in capability. A competent developer working with Claude Code or Codex could now replicate the core functionality of a mid-market SaaS product in weeks. Not perfectly, and not with every edge case handled, but well enough that the CIO reviewing a $500k annual renewal started asking the question: “what if we just built this ourselves?”

Every bear analyst in the room focused on what this meant for incumbents. The implications for ServiceNow and Zendesk and the long tail of SaaS were correctly identified and aggressively repriced. What almost nobody asked was what this meant for entrants.

A competent developer could replicate a mid-market SaaS product in weeks. But so could a former product manager with no engineering background. A laid-off financial analyst. A marketing director whose department had just been automated. The same tools that made it possible for enterprises to cancel their software contracts made it possible for individuals to build companies without raising venture capital, without hiring engineers, without the infrastructure cost that had historically made entrepreneurship the province of the well-funded.

We spoke with a procurement manager at a Fortune 500 in the summer of 2026 — the same procurement manager the bears would have recognized from their version of events: the one who forced a 30% discount on a SaaS renewal by credibly threatening to build the product internally. The bear narrative ends there. Ours does not.

Six months later, he left the Fortune 500. He built the internal tool. And then he packaged it, priced it at a 60% discount to the incumbent, and sold it to eleven other procurement teams in his industry — teams where he had relationships, where his credibility was real, where he understood the specific workflow pain points in ways that a general-purpose LLM could approximate but not replace. His total startup cost: $3,400 in AI inference and hosting fees. He has seventeen customers now and is hiring — two humans, because he needs people who understand the nuance of enterprise procurement in ways that remain, for now, human.

Multiply this dynamic by a few hundred thousand workers across every major metro. That is what the closed-loop model missed.

When the Floor Became a Launch Pad

The bear narrative correctly identified that displaced white-collar workers would not sit idle. It assumed they would downshift. Many did — and that part of the story was accurate and painful. But a remarkable number did something the models had not priced in. They started businesses.

This should not have been surprising. Prior technological disruptions have generated entrepreneurial booms in their wake. What was different this time was the sheer scale of barrier removal — and the quality of the cohort entering the market.

Starting a business in 2024 required capital, technical co-founders, legal infrastructure, accounting, HR, a sales team, office space. The fully-loaded cost of a ten-person startup in San Francisco was north of $3 million per year before it generated a dollar of revenue. The bottleneck was not ideas. It was friction.

By mid-2026, that friction was approaching zero. Legal incorporation: automated. Accounting: automated. Customer service: automated. Basic engineering: automated. Marketing copy, competitive analysis, financial modeling, contract review: automated. A motivated former white-collar professional with domain expertise and taste could launch a functional business in a weekend and reach their first hundred customers without a single full-time hire.

And the people entering this market were not average. These were workers who had cleared competitive hiring bars at demanding companies. Who had spent a decade accumulating domain expertise, professional networks, and the hard-won judgment about which problems were actually worth solving. What they had lacked was capital and technical infrastructure. They no longer needed either. Armed with AI tools that compressed months of execution into days, a single expert could now do what previously required a team of ten.

U.S. NEW BUSINESS FORMATIONS HIT 651,000 IN OCTOBER 2026, HIGHEST MONTHLY READING ON RECORD; SMALL BUSINESS ADMINISTRATION NOTES “STRUCTURAL ACCELERATION” IN SOLO AND MICRO-ENTERPRISE FILINGS | SBA / Census Bureau, November 2026

That October print was 40% above the prior record, set during the COVID-era stimulus boom. But unlike the 2020–2021 formation wave — which was dominated by gig-economy LLC filings and people trying to deduct home office expenses — this cohort was building real companies. Domain-specific AI wrappers targeting industries their founders had spent a decade in. Boutique consulting practices serving fifty enterprise clients with two humans and an agentic stack. Healthcare navigation services. Hyper-local service businesses with near-zero marginal cost of expansion.

The DoorDash story the bears told was accurate: coding agents had collapsed the barrier to launching a delivery app, fragmenting the market and compressing margins toward zero. But the same mechanism that destroyed DoorDash’s moat created dozens of profitable micro-logistics cooperatives — each run by a former gig worker who now owned the platform. The middle margin was not vaporized. It was redistributed. Not to machines, but to the network participants themselves.

The Deflationary Abundance That Actually Circulated

The bears coined “Ghost GDP” — output that shows up in national accounts but never circulates through the real economy. It was a compelling concept. But it rested on an assumption that deserved more scrutiny: that productivity gains would flow exclusively to capital and compute owners, never making their way to households.

Deflationary technologies do not work that way in competitive markets. They did not with electricity. They did not with the internet. They did not with containerization. In each case, the initial gains accrued to early adopters — and then competition distributed the surplus to consumers as cheaper goods and services. The velocity of money fell on the price side and rose on the volume side. The net was expansion.

Consider healthcare. The average American household spent $13,000 per year on healthcare in 2024 — a figure that, for tens of millions of families, functioned as a second mortgage. AI systems turned out to be extraordinarily capable at pattern recognition in clinical data. Diagnostic accuracy improved, administrative overhead collapsed, the cost of accessing specialist knowledge fell toward zero.

HEADLINE

U.S. HEALTHCARE CPI FALLS 4.2% Y/Y FOR SECOND CONSECUTIVE QUARTER; AI DIAGNOSTIC TOOLS AND ADMINISTRATIVE AUTOMATION CITED; KAISER NOTES 38% REDUCTION IN AVERAGE CLAIM PROCESSING COST | BLS / Kaiser Family Foundation, Q1 2028

A 4% annual decline in healthcare costs represents over $500 billion in real purchasing power returned to American households. Not Ghost GDP. Actual money that was previously flowing to a radiologist’s billing department, now available for literally anything else.

The same logic applied, with varying intensity, to legal services, financial planning, education, tax preparation, and home services. Every category where the service provider’s value proposition had been “I will navigate complexity you find tedious” got cheaper. The tens of millions of Americans who had never accessed a financial advisor because they could not afford one now had sophisticated financial planning available for $20 a month. They used it. That is new demand, conjured from suppressed demand that had always been there, waiting for the price to fall far enough.

We have been waiting two centuries for healthcare costs to decline in real terms. It took machine intelligence eighteen months. The bears asked how much money machines spend on discretionary goods. The right follow-up question was: how much more do humans spend when machines make everything cheaper?

There is a deeper flaw in the bear model that the GDP figures above do not fully capture. It is worth naming directly.

Cancer treatment costs the United States more than $200 billion annually. Every chemotherapy infusion, every imaging scan, every hospital admission — it all counts as GDP. The oncologists, the radiologists, the pharmaceutical manufacturers, the insurance administrators processing the claims: all employed, all spending their incomes, all nodes in the circular flow of money the bear model was so concerned to protect.

If we cured cancer overnight, we would “destroy” $200 billion in annual economic activity. The bear model, applied consistently, would have to count this as a catastrophe.

It is not a catastrophe. It is the point.

The destroyed activity was always a cost, not a benefit — a tax that disease levied on the productive economy. Eliminating it does not shrink the economy. It reallocates two hundred billion dollars toward anything else people would actually choose to spend on if disease did not consume their resources first. It returns millions of productive life-years. It frees capacity for conditions that remain unsolved. The caregiver burden — estimated at $25 billion annually in lost productivity — disappears from families and never makes it into the national accounts at all.

The bear model makes precisely this error with AI-driven efficiency. When a household’s legal fees drop from $8,000 to $240 a year, the $7,760 in savings does not disappear. It goes somewhere. When healthcare administration becomes 30% cheaper, the $258 billion in avoided costs does not exit the economy. It recirculates — into the discretionary spending, savings, and investment of the households that no longer have to pay it.

The bears counted the destruction. They forgot to count what humans do with what gets freed up. That omission is not a rounding error. It is the entire argument.

The Entrepreneurship Premium

There is a human story that cuts directly against the Salesforce PM narrative.

Our friend was a senior data scientist at a mid-sized insurance company in 2025. When the layoffs came in early 2027, she was in the third wave — initially spared because data scientists seemed useful for AI implementation. By the time the models could build and evaluate themselves, her role was gone. Title, health insurance, 401k, $160,000 a year.

She did not start driving for Uber.

She had spent four years watching her company’s underwriters make systematically poor decisions about a specific category of commercial real estate risk. She understood the patterns at a depth that no model trained on general data could replicate — because the patterns were embedded in the specific institutional history, the regional quirks, the informal relationships between underwriters and brokers that never made it into any training set. What she had lacked was the technical capacity to build the product and the capital to hire engineers. She no longer needed either.

Six months after her layoff, she launched a specialized commercial insurance analytics service. Her entire technical stack cost $800 a month. Her first client paid $4,000 a month. Her eighth client signed three weeks ago. She is on track to clear $380,000 this year — more than double her prior salary — working with two part-time human contractors who handle the client relationships that are, so far, still irreducibly human.

She represents a cohort the labor statistics struggled to capture, because she is not an employee. She does not appear in payroll data. She showed up, eventually, in self-employment income filings, in new business formations, in 1099 issuances. The BLS has been playing catch-up on measurement all year.

The labor market data looked catastrophic for six quarters because it was measuring the wrong things. Payroll employment fell. Self-employment income surged. The gap between the two was the story the consensus missed.

U.S. SELF-EMPLOYMENT INCOME SURGES 34% Y/Y IN Q4 2027; SOLO-OPERATOR BUSINESS REVENUES CROSS $1.4T ANNUALIZED; BLS NOTES “STRUCTURAL MEASUREMENT CHALLENGES” IN CURRENT HOUSEHOLD SURVEY METHODOLOGY | BLS / Census Bureau, January 2028

The new small business did not hire the way the old mid-sized company did. It needed one or two people with taste and domain knowledge, and machines for everything else. That is a different economy than the one we were modeled for — but it is not a broken one. It is, by several measures, a more equitable one. The returns to domain expertise and genuine judgment, previously pooled inside large organizations, were being distributed outward to the people who actually held them.

Policy Finds a Gear

We will not overstate this. The political process was, to use the technical term, a disaster.

The partisan gridlock was real. The Occupy Silicon Valley movement was real. The grandstanding was exhausting. The right called any transfer mechanism Marxism and warned that taxing compute would hand the lead to China. The left couldn’t agree on which intervention was least likely to become regulatory capture by incumbents. Fiscal hawks pointed at deficits. Everyone pointed at everyone else.

But two things happened that the pure gridlock scenario had not priced in.

First, state governments moved faster than the federal one. Several states — led, improbably, by Texas and Florida, which understood they were watching their income-tax-free advantage become a liability in a world of declining white-collar payroll — passed their own small business AI subsidy programs. Portable benefits that attached to individuals rather than employers. Retraining credits redeemable for AI tool subscriptions, not just accredited university tuition. These were not transformative policies. They were stabilizers, and timing mattered more than elegance.

Second, the federal government eventually passed something — just not what either side wanted. The Transition Economy Act that emerged from conference in March 2028 was smaller, messier, and more means-tested than any idealist had hoped. It included a modest inference compute tax, meaningful enough to fund direct transfers to displaced workers, too small to materially slow AI investment. It included expanded small business support, portable benefits infrastructure, and — buried in subsection 4(c) — a sovereign AI participation vehicle that nobody loved but nobody could kill.

It was not elegant. It did not solve the structural problem. What it did was buy time — six months of demand stabilization that allowed the entrepreneurship wave to compound and the deflationary effects to show up in the data. In a crisis driven by feedback loops, buying time is underrated. You only need to outlast the negative momentum long enough for the positive loops to establish themselves.

The canary they were watching did not die. It started a business.

From Sector Risk to Systemic Stability

Through 2027, markets treated the AI transition as a sector story going wrong — and then priced it, at peak fear in November 2027, as a systemic catastrophe. The crash that month was real. What the market was pricing in was a closed-loop model where displacement had no offset, and where the negative momentum would compound indefinitely.

As markets often do at peaks of fear, it was pricing in the absence of forces that were already in motion and not yet visible in lagging data.

Private credit did take real losses. Zendesk-style restructurings happened. The life insurer / Bermuda reinsurer architecture did draw regulatory scrutiny. The daisy chain of correlated bets on white-collar productivity growth unwound painfully. The bears were right about all of that — the mechanism was exactly as they described.

Where the catastrophe scenario broke down was in assuming these financial losses would transmit back into the real economy with the same force they had in 2008. In 2008, the losses were at the center of the credit system — in banks, in repo markets, in the instruments that funded overnight operations across the financial system. The contagion was instantaneous. In 2028, the losses were concentrated in closed-end vehicles with locked-up capital, held against long-duration insurance obligations. The system bent. It did not break.

The Fed cut rates aggressively. QE returned, targeting specifically the mortgage-adjacent markets. It did not solve the structural problem — a Claude agent genuinely can do the work of a $180,000 product manager for $200 a month, and that is not going to change. But it severed the transmission mechanism between the financial stress and the real economy just long enough for the entrepreneurship wave and the deflationary abundance to register in the data. By Q1 2028, the sentiment had turned before the fundamentals had fully confirmed it. That is how recoveries begin.

The Mortgage Question, Answered Differently

The 780 FICO borrower in San Francisco who lost her job in Q2 2027 was the central figure of the bear thesis. Her mortgage, underwritten against an income she could no longer reliably earn, was supposed to be the detonator that ignited a $13 trillion market.

Here is what actually happened to the borrower in our scenario.

Her income fell. She spent eight months in genuine uncertainty before landing on a mix of consulting engagements and a micro-SaaS product she had built over weekends. Her 2027 income was $95,000. Her 2028 income, annualized from Q1, is $140,000 and still rising.

But her monthly expenses fell in parallel. Healthcare through her employer had been costing $1,100 a month in premium and out-of-pocket. She now pays $280 for a plan with equivalent coverage, because AI-driven administration collapsed the overhead that had been consuming 30 cents of every premium dollar. Her financial planning, legal services for her LLC, and tax preparation — previously $8,000 a year in professional fees — cost her $240 a month in subscriptions.

The mortgage payment did not change. Everything around it got cheaper. She stayed current.

This is the deflationary offset the bear model did not build in. The same technology that compressed her nominal income compressed her cost of living. Not perfectly, not everywhere, not for everyone. But enough, at the median, to prevent the trajectory of mortgage delinquencies from becoming the 2008-style cascade the bears projected.

In 2008, the loans were bad on day one. In 2028, the loans were good on day one — and the world changed. But it changed in two directions simultaneously. Income pressure was real. So was cost relief. The bear model captured the first and ignored the second.

The Intelligence Premium Redistribution

The bears framed this as the unwind of the human intelligence premium. Machine intelligence was now a competent substitute for human intelligence across a growing range of tasks, and the premium repriced toward zero. That repricing was painful, disorderly, and far from complete.

We would frame it differently. The premium did not unwind. It redistributed.

What got cheaper was generic human intelligence — the ability to process information, draft communications, write code to specification, synthesize research. For fifty years, this work commanded significant wages because it was bottlenecked by the time and attention of people who had to sleep, take vacations, and navigate office politics.

What remained scarce — and became, arguably, more valuable precisely as generic intelligence became abundant — was everything that sat on top of it. Taste. Relationships. Domain credibility. The ability to know which problem to solve, not just how to solve it. The trust that a client places in a person, not a system.

Every previous moment in which a powerful tool became cheap and widely available created a new premium on the people who knew how to wield it with judgment. The printing press made literacy cheap and created a premium on original thought. The spreadsheet made calculation cheap and created a premium on strategic interpretation. Agentic AI made execution cheap and is creating a premium on taste, domain knowledge, and the human dimensions of commercial relationships.

The former Salesforce PM in the bear scenario became an Uber driver. In ours, she launched a product strategy consultancy targeting mid-market manufacturing companies — a sector she had spent eight years serving, whose workflow pain points she understood in ways that LLMs could approximate but not yet replace. Her AI tools make her ten times as productive as she was at Salesforce. They do not make her replaceable. They make her dangerous.

The Virtuous Loop

AI capability improves. Entrepreneurs launch businesses more cheaply. New demand is created at the edges of the economy, in niches that had never been economically viable to serve before. Those entrepreneurs hire — selectively, for judgment and relationships. Their businesses buy more AI capability. The cost of living falls as deflationary pressure propagates from category to category. Households find that real purchasing power is more stable than nominal income data suggests. AI capability improves.

This is not a stable equilibrium. It is a transition, and transitions are painful. There are real casualties. The legal sector shed 40% of its junior associate positions without replacing them. Traditional financial advisory is in structural decline. India’s IT services sector is in genuine crisis. These disruptions are not resolved.

The difference between our scenario and the bears’ is not that the disruption did not happen. It did. The difference is that it did not exhaust itself in a single direction. The same forces that destroyed jobs created the conditions for new ones. The same technology that made some businesses unviable made it possible to start new ones for $500 a month. The same deflationary pressure that compressed nominal wages expanded real purchasing power.

Doing the Math for the Other Half of the Ledger

The bear scenario presented its mechanism with quantitative precision. We will return the courtesy.

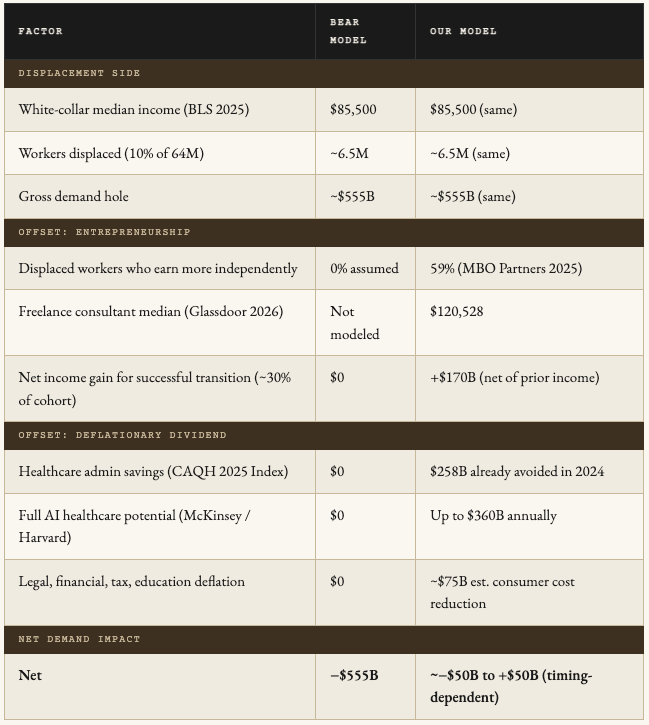

According to the Bureau of Labor Statistics, management, professional, and related occupations — the AI-vulnerable white-collar cohort — employ approximately 64 million workers at a median annual income of $85,500. A 10% displacement rate over 2026 and 2027 represents roughly 6.5 million workers and a nominal demand hole of approximately $555 billion. We accept this math. It is the starting point, not the conclusion.

The bear model then assumes those workers either stay unemployed or downshift into lower-wage work. Here is what the data says about that assumption.

The math roughly closes. But with honest caveats the bears would rightly demand: the timing is uneven — displacement is front-loaded and deflationary savings arrive on a lag. Distribution is lumpy — healthcare savings accrue broadly while displacement is concentrated in specific metros and job categories. Some workers fall through gaps that policy should close and doesn’t. Nominal GDP contracts even as real purchasing power expands, which is the source of the fear. The national accounts look worse than the lived economy feels.

The entrepreneurship offset deserves one additional layer of transparency. Not every displaced worker becomes a founder. The 59% figure from MBO Partners captures independents who successfully transition — it does not capture the roughly 40% who genuinely downshift, nor the significant fraction of new businesses that fail within 18 months. Our model assumes approximately 30% of the displaced cohort achieves a successful transition; the remaining 70% are carried by policy transfers, spousal income, or eventual re-employment. This is not a clean win for every worker. It is a net positive for the economy with real casualties that policy should address.

But the hole closes. And the mechanism that closes it is not government transfer or monetary stimulus. It is the same technology that opened it — deployed now by millions of domain experts who were liberated from institutional overhead and handed the most powerful productivity tools in history.

The bears built a model with one variable. The economy has two.

— — —

The output is still there. It is routing differently than it used to. The circular flow broke in some places and rebuilt in others. The disruption was real. The catastrophe was not.

The intelligence premium did not go to zero. It redistributed from credentials to judgment, from execution to taste, from the ability to do the work to the ability to know which work was worth doing.

The system was not designed for a disruption like this. Neither the tax code, nor the benefits system, nor the mortgage market, nor the labor statistics apparatus. All of them lagged reality by enough to generate real fear at the peak of uncertainty. But lag is not the same as failure. The system adapted — imperfectly, unevenly, and not without casualties — but it adapted.

The canary they were watching did not die.

It started a business.

But you are not reading this in June 2028. You are reading it in February 2026. The S&P is near all-time highs. The positive feedback loops have not begun. Neither have the negative ones. Both are coming. The question is not whether AI will disrupt the economy — it is whether the disruption generates a net positive or net negative equilibrium, and over what time horizon.

The difference between the two scenarios is not the technology. The technology is the same. The difference is what humans do with it, and to each other, in the years between now and then.

The canary is still alive. And it is starting to sing something we have not heard before.

In response to Citrini Research’s The 2028 Global Intelligence Crisis

These newsletters take significant effort to put together and are totally for the reader’s benefit. If you find these explorations valuable, there are multiple ways to show your support:

Engage: Like or comment on posts to join the conversation.

Subscribe: Never miss an update by subscribing to the Substack.

Share: Help spread the word by sharing posts with friends directly or on social media.

Humans have always panicked about technology. You see the same echos in the arguments from the printing press to now. Yet humans have always, and amazingly, adapted. Almost zero jobs remain today as they existed just 100 years ago and we are better for that.

Really enjoyed this. The cancer-as-GDP argument is one of those points that's obvious once someone says it and invisible until they do.

Where it gets tricky though: the whole model lives in the digital economy. The procurement manager's $3,400 startup works because software has near-zero marginal cost. But when you need robots, factories, supply chains, the barrier drops from $3M to maybe $300K, not $3,400. Still transformative, but way slower. The deflationary loop transmits fast in digital, slow in physical. The Intelligence Renaissance might arrive on very different timelines depending on which side of the atoms-vs-bits line you're on.

Also, love the "Intelligence Renaissance" framing. Beats the doom narratives by a mile.